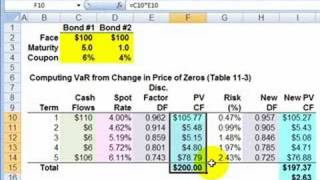

diversified bond value at risk (var)

Published 16 years ago • 17K plays • Length 8:59Download video MP4

Download video MP3

Similar videos

-

8:13

8:13

undiversified bond value at risk (var)

-

8:04

8:04

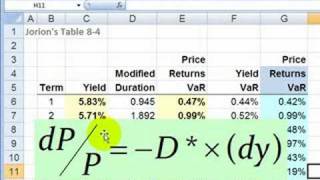

frm: bond returns value at risk (var) as bond risk

-

8:56

8:56

what is value at risk (var)? frm t1-02

-

19:44

19:44

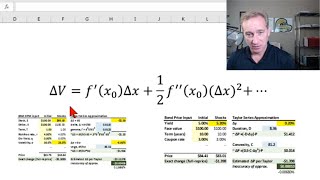

delta-gamma value at risk (var) with the taylor series approximation (frm t4-4)

-

5:30

5:30

frm: surplus at risk (pension var)

-

18:56

18:56

coherent risk measures and why var is not coherent (frm t4-5)

-

5:55

5:55

value at risk (var) explained in 5 minutes

-

22:29

22:29

value at risk (var) backtest (frm t5-04)

-

15:34

15:34

yield spread measures for fixed rate bonds - module 7 – fixed income– cfa® level i 2024 (and 2025)

-

10:05

10:05

marginal value at risk (marginal var)

-

5:55

5:55

frm: value at risk (var): historical simulation for portfolio

-

18:02

18:02

three approaches to value at risk (var) and volatility (frm t4-1)

-

21:26

21:26

value (var) mapping a fixed-income portfolio (frm t5-05)

-

26:41

26:41

lognormal value at risk (var, frm t5-01)

-

9:50

9:50

frm: intro to quant finance: value at risk (var)

-

21:57

21:57

var mapping (value at risk)

-

9:31

9:31

frm: liquidity adjusted value at risk (lvar)