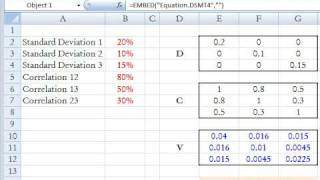

frm: how to get portfolio variance/var from the covariance matrix

Published 16 years ago • 62K plays • Length 10:00Download video MP4

Download video MP3

Similar videos

-

6:31

6:31

frm: covariance matrix

-

14:24

14:24

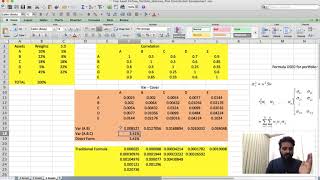

calculating portfolio variance using variance covariance matrix in excel risk contribution

-

9:54

9:54

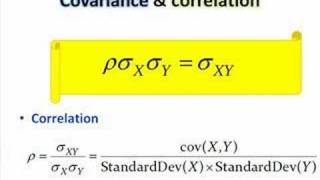

frm: correlation & covariance

-

19:46

19:46

portfolio variance-covariance matrix, return, and standard deviation for 3 securities on excel.

-

10:58

10:58

volatility: exponentially weighted moving average, ewma (frm t2-22)

-

15:59

15:59

option gamma (frm t4-15)

-

18:02

18:02

three approaches to value at risk (var) and volatility (frm t4-1)

-

11:00

11:00

the covariance matrix : data science basics

-

8:12

8:12

frm: mapping a fixed income portfolio (intro var mapping)

-

7:18

7:18

how to easily calculate portfolio variance for multiple securities in excel

-

5:55

5:55

frm: value at risk (var): historical simulation for portfolio

-

8:14

8:14

frm: var model backtest

-

7:11

7:11

frm: how to calculate (simple) historical volatlity