portfolio return and variance (calculations for cfa® and frm® exams)

Published 3 years ago • 9.7K plays • Length 21:19Download video MP4

Download video MP3

Similar videos

-

21:08

21:08

beta and capm (calculations for cfa® and frm® exams)

-

20:01

20:01

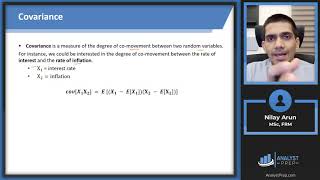

covariance and correlation (calculations for cfa® and frm® exams)

-

55:39

55:39

portfolio risk and return - part i (2024 level i cfa® exam – pm – module 1)

-

21:35

21:35

evolution of portfolio theory – from efficient frontier to cal to sml (for cfa® and frm® exams)

-

54:59

54:59

portfolio risk and return – part ii (2024 level i cfa® exam – pm – module 2)

-

19:48

19:48

sharpe ratio, treynor ratio and jensen's alpha (calculations for cfa® and frm® exams)

-

10:13

10:13

monte carlo method: value at risk (var) in excel

-

57:33

57:33

asset allocation to alternative investments – part i (2024 level iii cfa® – reading 19)

-

6:30

6:30

var (value at risk), explained

-

1:21:24

1:21:24

afm-portfolio theory and analysis

-

7:15

7:15

expected portfolio return from a joint probability function (for the @cfa level 1 exam)

-

4:07

4:07

portfolio variance for a two-asset portfolio (for the @cfa level 1 exam)

-

23:06

23:06

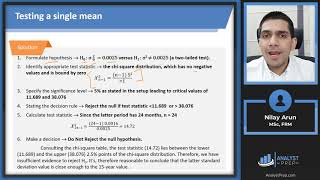

hypothesis testing (calculations for cfa® and frm® exams)

-

32:43

32:43

portfolio mathematics (2024 cfa® level i exam – quantitative methods – learning module 5)

-

3:29

3:29

calculating risk and return of a two asset portfolio

-

1:17:17

1:17:17

portfolio risk and return - part i (2023 level i cfa® exam – pm – module 2)

-

40:00

40:00

backtesting and simulation (2024 level ii cfa® exam –pm– module 4)

-

28:03

28:03

portfolio credit risk (frm part 2 2023 – book 2 – chapter 7)

-

19:37

19:37

timelines – your best friends (calculations for cfa® and frm® exams)

-

27:37

27:37

2015- frm part i - delineating efficient portfolios- part 1 (of 2)

-

20:59

20:59

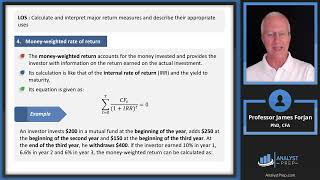

level i cfa pm: portfolio risk and return: part ii-lecture 1