stochastic calculus for quants | risk-neutral pricing for derivatives | option pricing explained

Published 2 years ago • 30K plays • Length 24:44Download video MP4

Download video MP3

Similar videos

-

7:40

7:40

stochastic volatility models used in quantitative finance

-

22:20

22:20

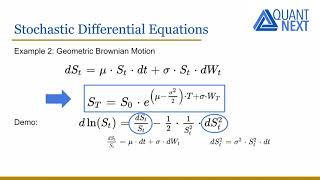

stochastic calculus for quants | understanding geometric brownian motion using itô calculus

-

7:03

7:03

introduction to stochastic calculus

-

4:57

4:57

how to get rich with calculus

-

16:44

16:44

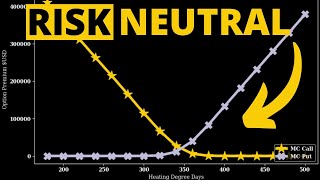

monte carlo simulation of temperature for weather derivative pricing

-

10:58

10:58

1.1 the binomial model - stochastic calculus for finance i

-

27:14

27:14

risk neutral pricing of weather derivatives

-

6:43

6:43

stock prices as stochastic processes

-

15:15

15:15

brownian motion for financial mathematics | brownian motion for quants | stochastic calculus

-

22:23

22:23

4 2 risk neutral pricing part 1

-

10:03

10:03

what is a quant? - financial quantitative analyst

-

10:12

10:12

risk neutral probability measure simplified

-

1:58

1:58

stochastic calculus by kamil zajac

-

19:05

19:05

modifying the ornstein-uhlenbeck process | a practical application of stochastic calculus for quants