bond dv01 and duration

Published 14 years ago • 67K plays • Length 6:31Download video MP4

Download video MP3

Similar videos

-

12:33

12:33

fixed income: bond dv01 (aka, price value of basis point, frm t4-32)

-

9:24

9:24

hedging with dv01

-

19:05

19:05

fixed income: impact of yield and coupon on duration and dv01 (frm t4-39)

-

15:10

15:10

fixed income: hedging the dv01 (frm t4-33)

-

8:59

8:59

what is the yield curve, and why is it flattening?

-

9:16

9:16

how can investing in bonds benefit retail investors? | strategies you can adopt | bonds simplified

-

4:56

4:56

bond maturity vs duration | bonds & bond funds

-

3:55

3:55

frm: treasury strips

-

6:41

6:41

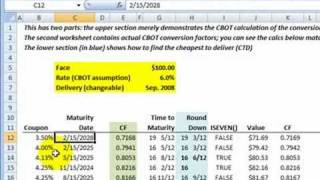

frm: treasury bond futures: conversion factor

-

5:55

5:55

frm: cheapest to deliver (ctd) treasury bond

-

7:30

7:30

frm: dollar duration of zero coupon bond

-

7:38

7:38

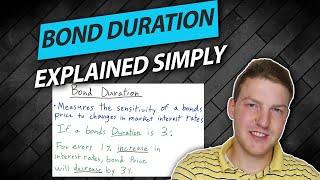

frm: bond duration (introduction)

-

5:07

5:07

bond duration explained simply in 5 minutes

-

45:33

45:33

applying duration, convexity, and dv01 (frm part 1 2023 – book 4 – chapter 12)

-

6:11

6:11

frm: catastrophe (cat) bond

-

19:17

19:17

fixed income: duration plus convexity to approximate bond price change (frm t4-38)

-

9:46

9:46

fixed income: maturity versus bond price (frm t4-26)