fixed income: maturity versus bond price (frm t4-26)

Published 5 years ago • 2.2K plays • Length 9:46Download video MP4

Download video MP3

Similar videos

-

19:17

19:17

fixed income: duration plus convexity to approximate bond price change (frm t4-38)

-

9:46

9:46

fixed income: bond spread (frm t4-28)

-

17:17

17:17

fixed income: yield to maturity (frm t4-29)

-

12:33

12:33

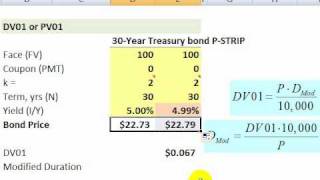

fixed income: bond dv01 (aka, price value of basis point, frm t4-32)

-

24:48

24:48

fixed income: bullet versus barbell bond portfolio (frm t4-40)

-

11:12

11:12

fixed income: term structure scenarios (frm t4-30)

-

19:43

19:43

fixed income: carry roll down (frm t4-31)

-

11:47

11:47

fixed income: modified and macaulay duration (frm t4-35)

-

15:10

15:10

fixed income: hedging the dv01 (frm t4-33)

-

16:33

16:33

fixed income: infer discount factors, spot, forwards and par rates from swap rate curve (frm t4-25)

-

6:31

6:31

bond dv01 and duration

-

12:41

12:41

fixed income: simple bond illustrating all three durations (effective, mod, mac) (frm t4-36)

-

15:08

15:08

fixed income: gross versus net realized return (frm t4-27)

-

6:10

6:10

closed-from (analytical) bond price formula

-

11:41

11:41

fixed income: bond's full/flat price on settlement date (frm t4-22)

-

9:12

9:12

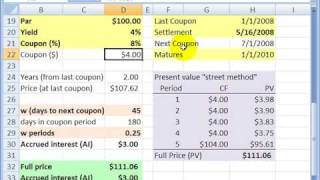

full versus flat bond price (aka, cash vs. quoted or dirty vs. clean price, frm t3-23)

-

7:41

7:41

accrued interest (clean versus dirty bond price)