frm: how to value an interest rate swap

Published 16 years ago • 255K plays • Length 9:14Download video MP4

Download video MP3

Similar videos

-

8:05

8:05

frm: interest rate swap (irs) valuation: as two bonds

-

7:04

7:04

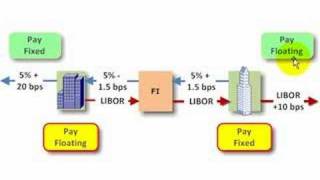

frm: interest rate swap

-

5:17

5:17

frm: swap rate versus spot rate

-

8:52

8:52

frm: forward rate agreement (fra)

-

9:22

9:22

comparative advantage in an interest rate swap (frm t3-31)

-

6:25

6:25

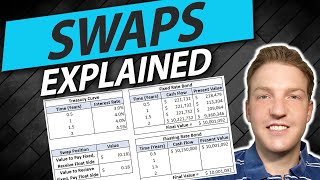

interest rate swaps explained | example calculation

-

9:25

9:25

frm: valuation of credit default swap (cds)

-

3:38

3:38

interest rate swap explained

-

5:07

5:07

bond duration explained simply in 5 minutes

-

9:52

9:52

forward rate agreement, fra (frm t3-12)

-

4:42

4:42

frm: currency swap

-

19:02

19:02

valuation of plain-vanilla interest rate swap (t3-32)

-

12:20

12:20

interest rate parity applies cost of carry model (frm t3-21)

-

8:16

8:16

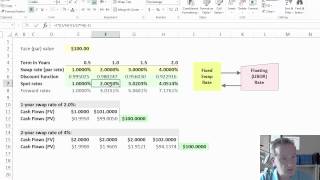

valuing an interest rate swap

-

18:27

18:27

fixed for fixed currency swap: mechanics and valuation (t3-33)

-

7:12

7:12

frm: why a futures price differs from a forward price

-

6:31

6:31

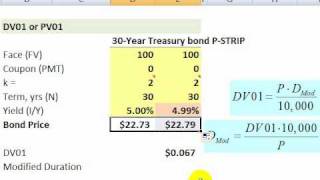

bond dv01 and duration

-

6:29

6:29

us t-bond futures cheapest to deliver (ctd, frm t3-26)

-

11:35

11:35

interest rates: compound frequencies (frm t3-8)

-

7:41

7:41

frm: counterparty credit exposure

-

7:36

7:36

interest rate parity: visual/mathematical (frm t3-21b)