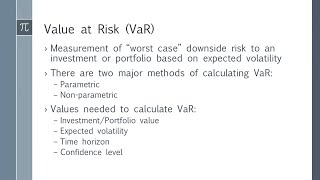

historical simulation method of measuring var | qms and its role in financial risk management

Published 1 month ago • 13 plays • Length 1:00Download video MP4

Download video MP3

Similar videos

-

0:47

0:47

disadvantage of historical simulation method of measuring var | qms and financial risk management

-

0:40

0:40

parametric & analytic method of measuring var | qms and its role in financial risk management

-

0:32

0:32

disadvantage of parametric and analytic method of measuring var | qms and financial risk management

-

5:01

5:01

historical method: value at risk (var) in excel

-

9:17

9:17

value-at-risk calculation - historical simulation

-

23:42

23:42

all about value at risk(var) | frm part 1 2023| historical simulation, delta normal, monte carlo var

-

8:49

8:49

what is the (basic) historical simulation approach to value at risk (var)? frm t1-5

-

13:42

13:42

value at risk in excel historical vs monte carlo methods

-

6:30

6:30

var (value at risk), explained

-

10:13

10:13

monte carlo method: value at risk (var) in excel

-

8:41

8:41

var thru monte carlo simulation

-

9:11

9:11

frm: historical simulation, value at risk (var)

-

5:10

5:10

frm: historical simulation value at risk (hs var)

-

19:37

19:37

historical simulation (hs var): basic and age-weighted (frm t4-2)

-

9:36

9:36

how to calculate value at risk (var) using excel || value at risk explained

-

22:24

22:24

value-at-risk (var) - variance-covariance and historical simulation methods (excel) (sub)

-

20:39

20:39

calculating and applying var (frm part 1 2023 – book 4 – valuation and risk models – chapter 2)

-

11:04

11:04

historical value-at-risk (var) and conditional var (cvar) in excel