volatility (frm part 1 2023 – book 2 – chapter 14)

Published 5 years ago • 3.9K plays • Length 14:44Download video MP4

Download video MP3

Similar videos

-

21:33

21:33

bayesian analysis (frm part 1 2023 – book 2 – chapter 4)

-

20:39

20:39

calculating and applying var (frm part 1 2023 – book 4 – valuation and risk models – chapter 2)

-

19:44

19:44

delta-gamma value at risk (var) with the taylor series approximation (frm t4-4)

-

7:06

7:06

frm: implied volatility

-

10:00

10:00

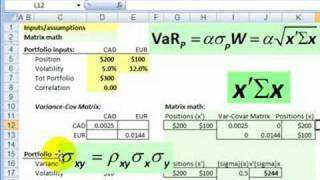

frm: how to get portfolio variance/var from the covariance matrix

-

33:18

33:18

estimating market risk measures (frm part 2 2023 – book 1 – chapter 1)

-

59:14

59:14

measuring and monitoring volatility in frm part 1 | var 2023

-

1:14:02

1:14:02

measuring and monitoring volatility | frm part i | 2021

-

27:24

27:24

probabilities (frm part 1 2023– book 2 – chapter 1)

-

50:51

50:51

correlation basics: definitions, applications, and terminology (frm part 2 – book 1 – chapter 7)

-

20:01

20:01

covariance and correlation (calculations for cfa® and frm® exams)

-

37:09

37:09

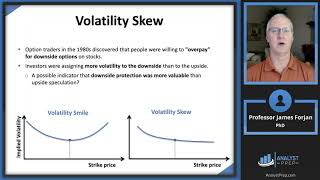

volatility smiles (frm part 2 2023 – book 1 – chapter 15)

-

17:10

17:10

2015 - frm : quantifying volatility in var models part i(of 2)

-

18:20

18:20

measures of financial risk (frm part 1 2023 – book 4 – chapter 1)

-

7:11

7:11

frm: how to calculate (simple) historical volatlity

-

48:31

48:31

measuring credit risk (frm part 1 2023 – book 4 – chapter 6)